Key Summary

For a long time, access to short-term funds in the United States has been closely tied to credit scores. If your score was strong, you were seen as reliable. If your score was low, or if you had no credit history at all, your options narrowed significantly. This created a system where financial access depended less on how you manage money today and more on how you have interacted with credit in the past.

In 2026, that gap is becoming more visible. Millions of people actively manage their finances without relying on traditional credit systems. Some are new to the country and have not yet built a credit file. Others have faced financial setbacks in the past that impacted their scores but have since stabilized their income and spending. There are also users who intentionally avoid credit and prefer to operate within a cash flow model, relying on what they earn and manage in real time.

The challenge for all these users is not financial irresponsibility. It is the inability of traditional systems to recognize financial behavior that exists outside credit history.

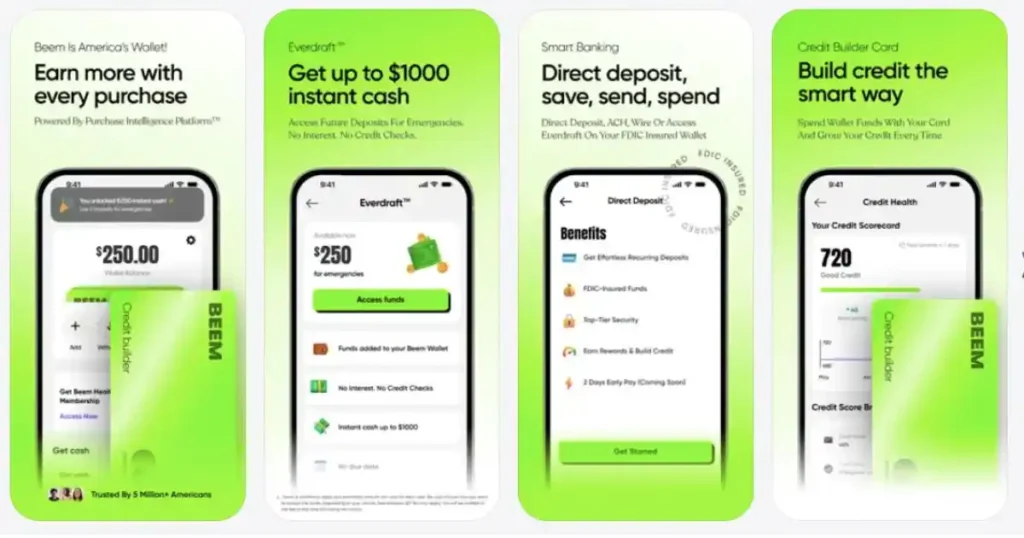

This is where Beem introduces a different framework. Through Everdraft™, it allows users with bad credit or no credit to access cash advances by evaluating their current financial activity rather than relying on credit scores.

Why Traditional Systems Struggle With Bad or No Credit Profiles

Credit Scores Are Built on Borrowing History

Credit scoring models are designed to assess how individuals have handled borrowed money over time. They track repayment consistency, outstanding debt, and the length of credit history. This creates a structured way to measure risk for lenders.

However, this structure assumes that everyone has participated in the credit system. If you have never used credit, there is little or no data to evaluate. If your past includes missed payments or financial hardship, that history can continue to affect your score long after your situation has improved.

The Gap Between Past and Present Financial Reality

One of the biggest limitations of credit-based systems is that they rely on historical data. They do not always reflect your current financial situation.

A user may have a low credit score due to past challenges but now maintain steady income and disciplined spending. Another user may have no credit history but manage their finances responsibly every day. In both cases, traditional systems may fail to recognize present stability.

How Beem Changes the Evaluation Model

Beem shifts the focus from historical credit data to real-time financial behavior.

Instead of asking whether you have borrowed and repaid in the past, it evaluates how you manage your finances today. This includes analyzing patterns in deposits, account activity, and spending behavior over time.

This approach allows the platform to identify stability even when it does not appear in traditional credit reports. It creates a pathway for users to access financial tools based on current behavior rather than past limitations.

What Everdraft™ Looks at Instead of Your Credit Score

Consistency of Income, Regardless of Source

Everdraft™ evaluates whether money is entering your account regularly. This does not need to come from a single employer or follow a fixed schedule. Income from freelance work, gig platforms, transfers, or multiple sources can all contribute to a consistent pattern.

The key factor is continuity. Even if deposits vary in size or timing, regular inflows indicate that your financial system is active.

Frequency and Quality of Account Activity

An active bank account provides valuable insight into how you manage money. Frequent transactions, bill payments, and everyday spending patterns show that your financial life is ongoing and engaged.

This activity helps build a clearer picture of how you interact with your finances on a daily basis.

Balance Stability and Cash Flow Management

Everdraft™ also evaluates how well you manage your account balance over time. Large and unpredictable fluctuations may indicate instability, while more controlled patterns suggest thoughtful financial management.

Maintaining a balance between inflows and outflows is an important signal of reliability.

Spending Behavior and Financial Discipline

How you spend your money is just as important as how you earn it. Consistent spending patterns, avoidance of extreme fluctuations, and responsible use of funds all contribute to a stronger financial profile.

These behaviors demonstrate discipline, which is a key factor in determining eligibility.

Continuity Across Time

Short-term activity is not enough to establish stability. Everdraft™ looks for patterns that persist over weeks and months. This continuity provides a more accurate representation of financial behavior.

Why This Model Works for Users With Bad Credit

It Separates Past Mistakes From Present Behavior

A low credit score often reflects past financial challenges. However, it does not always represent how you are managing money today.

Beem’s model allows users to demonstrate their current financial stability without being limited by historical data. This creates an opportunity to access funds based on present behavior.

It Recognizes Financial Recovery

Many users improve their financial habits over time. They stabilize their income, manage expenses more effectively, and build better financial routines.

Behavior-based evaluation captures this improvement, allowing users to move forward rather than being held back by past records.

Why This Model Works for Users With No Credit History

It Removes the Need for Prior Participation

Traditional systems require a credit history to evaluate eligibility. Without it, users are often excluded.

Beem removes this barrier by focusing on financial activity rather than credit history. This allows users to demonstrate reliability without needing to borrow first.

It Creates an Entry Point Into Financial Access

For new users, Everdraft™ provides a way to access funds based on current behavior. This can be particularly valuable for individuals who are just beginning to establish their financial presence.

Read: How to Avoid Hidden Fees in Instant Cash Advance Apps

How to Strengthen Your Eligibility Without Credit

Maintain Consistent Deposits

Even if your income varies, regular deposits help create a recognizable pattern over time.

Keep Your Account Active

Frequent transactions and ongoing activity provide more data for evaluation.

Manage Spending Thoughtfully

Balanced spending and controlled withdrawals demonstrate financial discipline.

Avoid Long Periods of Inactivity

Consistent engagement helps maintain visibility and strengthens your profile.

Comparing Credit-Based vs Behavior-Based Access

| Factor | Credit-Based Systems | Beem (Everdraft™) |

| Evaluation Basis | Past credit history | Current financial behavior |

| Credit Score Required | Yes | No |

| Accessibility | Limited by history | Broad and inclusive |

| Flexibility | Low | High |

| Adaptability | Static | Dynamic |

The Bigger Shift in Financial Access

The ability to access funds without relying on credit scores reflects a broader transformation in financial systems.

Income is becoming more dynamic. Financial behavior is increasingly real-time. Users are managing money actively rather than relying solely on long-term credit structures.

By focusing on behavior instead of history, Beem aligns its model with how people actually manage money today.

How Financial Behavior Creates a Second Path to Access

For a long time, credit history has been the only recognized pathway to financial access. If you participated in the credit system, you could build eligibility. If you did not, or if your history was damaged, your options became limited. Behavior-based models introduce a second pathway, one that is built on how you manage money in real time.

This alternative path is important because it shifts control back to the user. Instead of being dependent on past borrowing activity, you can build eligibility through consistent deposits, active account usage, and disciplined spending. Over time, this creates a parallel system of trust that operates independently of traditional credit scores.

Why Financial Recovery Should Not Be Penalized Indefinitely

Many people who have low credit scores are not financially unstable in the present. Their scores often reflect past challenges such as missed payments, temporary income disruptions, or unexpected expenses. While these events are part of their financial history, they do not necessarily define their current behavior.

Behavior-based systems allow for a more balanced view. By focusing on present activity, they recognize improvement and recovery. This ensures that users are not indefinitely penalized for past circumstances and can regain access based on how they manage their finances today.

The Role of Cash Flow Awareness in Eligibility

Cash flow awareness is the ability to understand how money moves in and out of your account over time. It involves knowing when income arrives, how expenses are distributed, and how balances fluctuate.

In behavior-based evaluation, this awareness becomes a key factor. Users who actively manage their cash flow, ensuring that expenses align with income and that balances remain stable, create stronger financial patterns. These patterns signal reliability because they reflect intentional financial management rather than reactive decision-making.

How Multi-Source Income Strengthens Your Profile

Traditional systems often struggle with multiple income sources because they expect a single, consistent paycheck. Behavior-based systems interpret this differently.

Multiple income streams can actually strengthen your financial profile when viewed collectively. They show diversification, which can indicate resilience. If one source fluctuates, others may compensate, creating a stable overall pattern.

This aggregated stability is particularly relevant in 2026, where diversified income is becoming more common across different professions and lifestyles.

Why Financial Visibility Is Just as Important as Financial Stability

You may be financially stable, but if your activity is not visible within your bank account, the system has limited information to work with. Visibility ensures that your income and spending patterns can be accurately interpreted.

This means routing deposits through your account, maintaining consistent transaction records, and avoiding fragmented financial activity across multiple untracked channels. Visibility transforms financial behavior into data that can be evaluated, making it a critical component of eligibility.

The Impact of Short-Term Consistency vs Long-Term Patterns

Short-term consistency can create a positive impression, but it is long-term patterns that build trust. A few weeks of stable activity may not be enough to establish reliability, but consistent behavior over several months creates a stronger foundation.

Behavior-based systems place significant emphasis on this continuity. They look for patterns that persist over time, as these are more reliable indicators of financial stability. This reinforces the importance of maintaining consistent habits rather than focusing on short-term adjustments.

How Financial Discipline Becomes the New Qualification Standard

In credit-based systems, qualification is often tied to external metrics such as credit scores and income thresholds. In behavior-based systems, discipline becomes the defining factor.

Consistent spending, controlled withdrawals, and thoughtful financial decisions all contribute to a stronger profile. These behaviors demonstrate that you are managing your finances responsibly, which is ultimately what lenders and financial platforms are trying to assess.

This shift places greater emphasis on how you handle money rather than how your financial history is recorded.

The Long-Term Benefits of Behavior-Based Financial Access

Accessing financial tools through behavior-based systems does more than solve immediate needs. It also encourages better financial habits over time.

As users become more aware that their eligibility is tied to consistency, visibility, and discipline, they begin to manage their finances more intentionally. This creates a positive feedback loop where better behavior leads to improved access, which in turn reinforces stronger habits.

Over time, this can lead to a more stable and sustainable financial life, independent of traditional credit systems.

Conclusion

Having bad credit or no credit no longer has to be a barrier to accessing financial tools. Through Everdraft™, Beem provides a way to access cash advances based on how you manage your finances today, not how you have borrowed in the past.

This approach creates a more inclusive and accurate system, allowing users to demonstrate reliability through real-world financial behavior.

FAQs

1. Can I really qualify for Everdraft™ if I have a very low credit score?

Yes, you can. Beem does not rely on your credit score to determine eligibility. Instead, it evaluates your current financial activity, including how consistently you receive income, how actively you use your account, and how stable your spending patterns are. Even if your credit score is low due to past financial challenges, you can still qualify if your present financial behavior demonstrates stability and discipline.

2. What if I have never used credit before? Will I still be eligible?

Yes, having no credit history does not prevent you from qualifying. Beem’s model is specifically designed to include users who have not participated in traditional credit systems. By focusing on real-time financial activity, it allows you to demonstrate reliability through how you manage money rather than through past borrowing.

3. How does Beem determine how much I can access without a credit score?

The amount you can access, up to $1,000, is determined by your financial profile. This includes factors such as the consistency of your deposits, the frequency of your account activity, and the stability of your spending patterns. The system evaluates how strong and continuous your financial behavior is over time.

4. Will using Everdraft™ help improve my credit score?

Everdraft™ does not directly impact your credit score because it does not report to credit bureaus. However, it allows you to manage short-term financial needs without relying on traditional credit products, which can help you maintain overall financial stability.

5. Is this approach safer than relying on credit-based systems?

This approach is not necessarily safer or riskier, but it is more aligned with real-time financial behavior. By focusing on how you manage money today, it provides a more current and flexible evaluation. For users with bad or no credit, this can be a more accurate and accessible way to access financial tools.