Key Summary

For years, the idea of cash advance has been tightly linked to your credit score. It has been treated as the single most important signal of whether you are “eligible” or not. A strong score opened doors. A limited or poor score often closed them before the conversation even began.

But that framework assumes something that is no longer universally true. It assumes that past borrowing behavior is the best way to judge present financial responsibility. In 2026, that assumption is being re-evaluated.

A large and growing group of users manage their finances without relying heavily on credit. Some are new to the U.S. and have not yet built a credit profile. Others actively avoid debt and prefer to operate within their means. Many earn through multiple sources and manage money dynamically, adjusting to real-time needs rather than fixed repayment cycles.

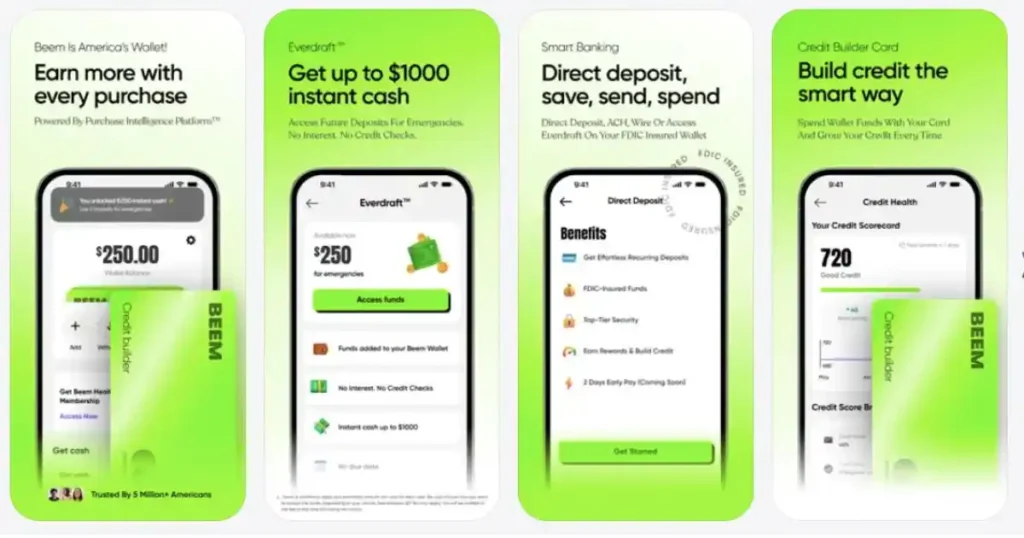

For these users, the issue is not capability. It is recognition. This is where Beem offers a different path. Through Everdraft™, it provides cash advance without a hard credit check by evaluating how money is actually managed today, not how it was borrowed in the past.

Why Credit Scores Became the Default in Lending

A Standardized System for Scale

Credit scores were introduced as a way to simplify lending decisions. By converting complex financial histories into a single number, lenders could quickly assess risk across large populations.

This made it easier to:

- Compare applicants consistently

- Automate approval processes

- Reduce uncertainty in long-term lending

For products like mortgages and large loans, this system still plays an important role because it reflects long-term repayment behavior.

The Trade-Off of Simplification

However, reducing financial behavior to a single score comes with limitations. It overlooks nuance. It does not account for current income changes, evolving financial habits, or non-credit-based financial activity.

A user may be financially disciplined but have no credit history. Another may have a strong score but struggle with present-day cash flow. In both cases, the score does not tell the full story.

How Behavioral Data Creates a More Complete Financial Profile

One of the key advantages of moving away from credit scores is the ability to build a more complete and layered understanding of financial behavior. Credit reports focus primarily on borrowing, repayment, and outstanding debt. While this is useful, it captures only one dimension of a person’s financial life.

Behavior-based systems expand this view. By analyzing deposits, withdrawals, spending patterns, and account activity, platforms like Beem create a multi-dimensional profile. This profile reflects how money is earned, how it is used, and how consistently it flows over time.

This broader perspective allows for a more accurate assessment of financial stability, especially for users who do not rely heavily on traditional credit.

Why Real-Time Financial Snapshots Are More Relevant Than Historical Records

Credit scores are built on historical data, which may not always reflect current realities. A user’s financial situation can change significantly in a short period, whether due to new income sources, changes in expenses, or shifts in financial priorities.

Real-time financial snapshots provide a more current view. They capture what is happening in your account now, not what happened months or years ago.

This immediacy makes evaluation more relevant. It ensures that decisions are based on present conditions rather than outdated information, which is particularly important for short-term financial tools.

The Importance of Financial Momentum

Momentum is an often-overlooked aspect of financial behavior. It refers to the ongoing movement of money through your account and the consistency of that movement over time.

An account with steady inflows and regular activity demonstrates forward momentum. This indicates that your financial system is active and sustainable.

Even if individual transactions vary, maintaining this momentum helps build a stronger profile. It shows that your financial life is not static but continuously evolving in a stable manner.

How Smaller, Frequent Deposits Can Strengthen Your Profile

Many users assume that larger deposits carry more weight in financial evaluation. While size does matter, frequency often plays a more important role in behavior-based systems.

Smaller, frequent deposits create a detailed activity trail. They show consistent engagement and provide more data points for analysis. This makes it easier for the system to identify patterns and establish reliability.

For gig workers and freelancers, this can be a significant advantage. Their income structure naturally aligns with this type of activity, allowing them to build strong profiles without needing large, uniform payments.

The Role of Financial Visibility in Eligibility

Visibility is a critical factor in behavior-based evaluation. If your financial activity is not clearly reflected in your bank account, the system has limited information to work with.

This means that even if you are earning consistently, fragmented or off-record income can reduce your eligibility. Ensuring that deposits are routed through your account helps create a clear and traceable financial record.

Visibility turns financial activity into usable data, which is essential for accurate evaluation.

How Consistency Builds Trust Over Time

Trust in financial systems is not established instantly. It develops as patterns become more consistent and predictable over time.

Each week of steady activity, each month of balanced inflows and outflows, adds to your financial track record. Over time, this consistency reduces uncertainty and strengthens your profile.

This gradual process is important to understand. Eligibility is not just about meeting a threshold. It is about building a history of reliable behavior.

Why Behavior-Based Systems Are More Inclusive by Design

Traditional credit systems tend to exclude users who do not fit established patterns. This includes individuals with limited credit history, irregular income, or non-traditional financial roles.

Behavior-based systems are inherently more inclusive because they focus on what users are doing now rather than what they have done in the past. They allow for multiple pathways to demonstrate stability.

This inclusivity is not about lowering standards. It is about expanding the definition of what financial reliability looks like.

The Long-Term Impact of Moving Beyond Credit Scores

The shift away from credit scores is not just a short-term trend. It represents a broader transformation in how financial systems operate.

As more platforms adopt behavior-based evaluation, users will have greater control over their financial access. They will be able to build eligibility through consistent activity and responsible management rather than relying solely on historical credit data.

Over time, this could lead to a more balanced financial ecosystem, where access is determined by real-world behavior rather than rigid scoring systems.

What “No Credit Check” Actually Means in Practice

No Hard Inquiry Into Your Credit File

When Beem says it does not perform a credit check, it specifically means there is no hard inquiry made into your credit report. This ensures that your credit score is not impacted in any way by using the platform.

This is particularly important for users who are cautious about maintaining their credit profile or who want to avoid unnecessary inquiries.

A Shift in How Evaluation Happens

Removing the credit check does not eliminate evaluation. It changes the foundation of that evaluation.

Instead of relying on external credit data, Beem analyzes internal financial activity. It looks directly at how your money moves, how often it appears, and how it is managed over time. This creates a profile that is rooted in present behavior rather than historical borrowing.

Read: Beem Credit Builder: How It Helps First-Time Borrowers

What Beem Looks at Instead of Your Credit Score

Beem evaluates a combination of behavioral signals that together form a detailed picture of financial stability.

Consistency of Deposits Over Time

Rather than focusing on a single income source, Beem looks at whether money is entering your account regularly. This could come from multiple sources, and that is acceptable.

What matters is that there is continuity. Even if deposits vary in size or timing, consistent inflows indicate that your financial system is active and functioning.

Frequency and Depth of Account Activity

An account that is actively used provides more insight than one that is dormant. Regular transactions, bill payments, and spending activity show that you are engaged with your finances on an ongoing basis.

This activity helps the system understand how you interact with your money, not just how you receive it.

Balance Stability and Cash Flow Management

Your account balance tells a story about how well inflows and outflows are managed. Large, unpredictable swings may indicate instability, while a more controlled balance suggests that spending is aligned with income.

Beem evaluates this balance over time to determine whether your financial system is sustainable.

Spending Behavior and Financial Discipline

How you spend your money is just as important as how you earn it. Consistent spending patterns, avoidance of extreme fluctuations, and thoughtful financial decisions all contribute to a stronger profile.

This reflects discipline, which is a key indicator of reliability.

Continuity Across Weeks and Months

Short-term activity can be misleading. A single week of strong deposits does not necessarily indicate long-term stability. Beem looks at patterns that persist over extended periods. Continuity across weeks and months provides a more accurate picture of how your finances operate.

Additional Signals That Strengthen Your Profile

Regularity of Income Sources

Even if income comes from multiple places, having recurring sources helps create predictability within variability. This strengthens the overall pattern.

Absence of Prolonged Inactivity

Gaps in account activity can make it harder to interpret financial behavior. Maintaining consistent engagement helps build a clearer profile.

Relationship Between Income and Expenses

When spending aligns with income over time, it indicates balance. This relationship is a strong signal of financial control.

How the Approval Process Works Step by Step

Step 1: Account Setup and Bank Linking

You begin by creating an account with Beem and linking your bank account. This step allows the system to access your financial data securely.

Step 2: Data Aggregation and Pattern Analysis

The platform analyzes your financial activity, identifying trends in deposits, spending, and account usage. This process focuses on patterns rather than isolated events.

Step 3: Building a Behavioral Financial Profile

Based on the data, Beem constructs a profile that reflects your financial habits. This profile evolves as your activity continues.

Step 4: Eligibility Determination for Everdraft™

If your profile demonstrates sufficient stability and continuity, you become eligible for Everdraft™. The system determines how much you can access based on your financial patterns.

Step 5: Access to Funds Without Credit Impact

Once approved, you can access up to $1,000 in instant cash without interest and without affecting your credit score.

Why This Model Works Better for Many Users

It Reflects Current Financial Reality

By focusing on real-time activity, Beem captures how users are managing money today. This is more relevant than relying solely on past borrowing behavior.

It Removes Historical Barriers

Users with limited or no credit history are not penalized. They can demonstrate stability through their current financial patterns.

It Adapts to Changing Circumstances

As your income and spending evolve, your financial profile updates accordingly. This creates a system that grows with you rather than locking you into past data.

Comparing Credit-Based vs Behavior-Based Evaluation

| Factor | Credit-Based Systems | Beem (Everdraft™) |

| Evaluation Focus | Past borrowing history | Current financial behavior |

| Credit Check | Required | Not required |

| Accessibility | Limited by credit history | Broad and inclusive |

| Flexibility | Low | High |

| Adaptability | Static | Dynamic |

A Shift From Scores to Real Financial Behavior

The move away from credit checks represents a broader evolution in financial systems. Instead of relying on a single numerical score, platforms are beginning to evaluate users based on how they actually manage money.

This shift recognizes that financial reliability is not just about past borrowing. It is about present behavior, ongoing patterns, and consistent management.

Conclusion

A no-credit-check cash advance does not mean there is no evaluation. It means the evaluation is more aligned with how financial life actually works.

Through Everdraft™, Beem assesses your financial behavior in real time, looking at deposits, spending, and account activity instead of relying on your credit score.

In 2026, this approach offers a more accurate, inclusive, and practical way to access financial tools, especially for users whose financial lives do not fit traditional credit models.

FAQs

1. If there is no credit check, how does Beem decide if I qualify?

Beem evaluates your financial behavior directly by analyzing your bank account activity. This includes how often money enters your account, how consistently you use it, and how stable your spending patterns are over time. Instead of relying on a credit score, it builds a profile based on real-time financial data, which provides a more current and practical measure of reliability.

2. Can I qualify even if I have a very low credit score?

Yes, your credit score does not play a role in determining your eligibility for Everdraft™. Even if your score is low or has been affected by past financial challenges, you can still qualify as long as your current financial activity demonstrates consistency and stability.

3. What if I have never used credit before?

You can still qualify without any credit history. Beem’s model is specifically designed to include users who are new to credit systems. By focusing on your present financial behavior, it allows you to demonstrate responsibility without needing a history of borrowing.

4. Does Beem check my credit in any indirect way?

No, Beem does not rely on your credit report for evaluation. It does not perform a hard inquiry or use your credit score as part of its decision-making process. All evaluation is based on your bank account activity and financial patterns.

5. Will using Everdraft™ help improve my credit score?

Everdraft™ does not directly impact your credit score because it does not report to credit bureaus. However, it can help you manage short-term financial needs without relying on traditional credit products, which may indirectly support better financial stability over time.