Key Summary

For a long time, access to cash advances in the United States has been built around a very specific assumption. If your income flows through a payroll system and lands in your bank account via direct deposit, you are considered financially predictable. If it does not, your eligibility becomes uncertain, limited, or in many cases, nonexistent.

That assumption shaped an entire category of financial apps. It created a system where access was tied more to how income looked than how it functioned. In 2026, that model is increasingly out of step with reality.

A growing number of people earn in ways that do not resemble traditional employment. Freelancers receive payments from multiple clients. Gig workers earn daily or weekly through platforms. Entrepreneurs manage irregular inflows tied to business cycles. Families often operate with shared financial systems where income and spending are not confined to one individual.

In each of these cases, financial activity is real, consistent, and actively managed. What is missing is not stability, but a system that can recognize it.

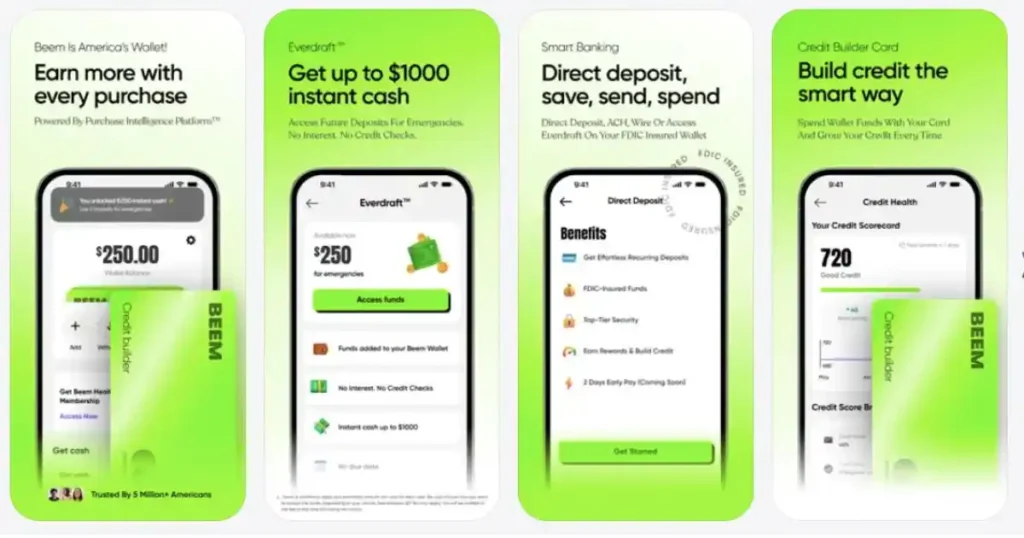

This is where Beem stands out among cash advance apps that do not require direct deposit. Through Everdraft™, it does not simply remove a requirement. It replaces the underlying logic, shifting from payroll-based evaluation to behavior-based interpretation.

Why Direct Deposit Became the Default Standard

Predictability as the Foundation of Traditional Models

Cash advance apps are built around risk management. When a platform provides access to funds, it needs to understand when those funds are likely to be repaid. Direct deposit simplifies this process by creating a predictable pattern.

A fixed paycheck provides clear signals. The system knows when income will arrive, how frequently it appears, and how much to expect. This allows it to align advances with repayment cycles efficiently.

The Limitation of a Single-Signal Approach

While this model is effective, it is also narrow. It assumes that predictability only exists in uniform patterns. It does not account for the fact that stability can emerge from multiple sources, varying timelines, and aggregated income streams.

As a result, many users who manage their finances responsibly are excluded simply because their income does not fit a predefined format. The system is not identifying risk accurately. It is filtering based on structure.

The Emergence of No-Direct-Deposit Cash Advance Apps

Moving From Structure to Behavior

As income patterns have evolved, some platforms have begun to move away from strict direct deposit requirements. Instead of relying on payroll data alone, they evaluate broader financial behavior.

This includes analyzing how frequently money enters an account, how consistently it is used, and how spending patterns reflect financial control. The goal is to build a more complete picture rather than relying on a single indicator.

Why This Shift Matters

For users with non-traditional income, this shift is not just convenient. It is essential. It allows them to access financial tools based on how they actually manage money, rather than how their income is labeled. This represents a more accurate and inclusive approach to financial evaluation.

What Sets Beem Apart From Other Apps in This Category

Beem is not simply an app that relaxes direct deposit requirements. It is designed from the ground up to function without relying on them.

A Fully Behavior-Based Evaluation Model

Beem evaluates your financial activity holistically. It looks at patterns that emerge over time rather than isolated transactions. This allows it to recognize stability even when income is distributed across multiple sources.

No Interest and No Credit Checks

Through Everdraft™, users can access up to $1,000 in instant cash without interest and without traditional credit checks. This removes two significant barriers that often limit access in other platforms.

Built for Modern Financial Complexity

Beem’s model is designed to handle real-world financial scenarios. It accommodates users with mixed income streams, irregular deposit schedules, and non-traditional financial roles. This is not an adaptation of an old system. It is a different system altogether.

How Beem Evaluates Stability Without Direct Deposit

Recognizing Patterns Instead of Labels

Traditional apps rely on labels such as “salary” or “payroll.” Beem focuses on patterns. If your account shows consistent inflows over time, regardless of source, it interprets that as stability.

Understanding Continuity Over Time

The system looks at how your financial activity evolves across weeks and months. It identifies whether there is ongoing movement and whether that movement reflects a functioning financial system.

Integrating Spending Behavior Into Evaluation

Income alone does not define stability. How that income is used also matters. Balanced spending, controlled withdrawals, and consistent account management all contribute to a stronger financial profile.

Read: Which Cash Advance Apps Support Cash App Withdrawals in 2026?

Who Benefits Most From No-Direct-Deposit Apps Like Beem

Freelancers and Independent Professionals

Multiple income streams can create a stable overall pattern, even if individual payments vary.

Gig Workers With Variable Earnings

Frequent deposits, even in smaller amounts, can establish continuity that reflects ongoing financial activity.

New Users Without Established Payroll Systems

Individuals who are new to the U.S. or just starting out financially can access tools without waiting to establish direct deposit.

Household Financial Managers

Stay-at-home parents or individuals managing shared finances can demonstrate stability through account activity rather than personal income labels.

Comparing Beem With Other Cash Advance Apps

| Factor | Traditional Apps | No-Direct-Deposit Apps | Beem (Everdraft™) |

| Direct Deposit Requirement | Mandatory | Optional | Not required |

| Evaluation Method | Payroll-based | Mixed | Fully behavior-based |

| Credit Check | Often required | Sometimes | Not required |

| Flexibility | Low | Moderate | High |

| Accessibility | Limited | Broader | Broadest |

This comparison highlights an important distinction. While some apps are beginning to adapt, Beem is built entirely around a different evaluation model.

The Role of Your Bank Account in a Behavior-Based System

Without direct deposit, your bank account becomes the central source of financial insight.

Visibility Becomes Critical

All income, regardless of source, needs to be reflected in your account. This ensures that your financial activity can be accurately interpreted.

Consistency Builds Confidence

Regular deposits, ongoing transactions, and stable usage patterns create a track record that strengthens your profile over time.

Activity Replaces Structure

In the absence of payroll signals, consistent activity becomes the primary indicator of financial stability.

How “Eligibility Signals” Work Without Payroll

In a payroll-based system, eligibility is largely determined by one dominant signal: your paycheck. In a behavior-based system, eligibility is built from multiple smaller signals that work together. These include deposit frequency, account activity, balance stability, and spending behavior.

Individually, these signals may not seem as strong as a fixed paycheck. Collectively, they create a detailed picture of how your finances operate. Over time, this layered evaluation becomes more reliable than a single-source model because it captures a broader range of financial behavior rather than relying on one pattern.

Why Frequency of Activity Can Outweigh Income Size

One of the most common misconceptions is that higher income automatically improves access. While income level does matter, behavior-based systems often prioritize frequency over size.

An account that shows regular deposits, even in smaller amounts, demonstrates ongoing financial activity. This continuous movement is easier to interpret than occasional large deposits, which may appear inconsistent. For many users, especially gig workers and freelancers, this works in their favor because it reflects the true nature of their income flow.

Read: How Beem Verifies Income for Gig and Freelance Workers Without an Employer

The Advantage of Aggregated Financial Stability

Traditional systems evaluate income in isolation. Each deposit is judged on its own, without considering how it contributes to a larger pattern.

Behavior-based systems like Beem’s take a different approach by aggregating financial activity. Multiple smaller income streams, when viewed together, can create a stable overall pattern. This is particularly important in 2026, where diversified income is becoming more common.

This aggregated view allows users to demonstrate stability even when individual transactions appear irregular.

How Spending Discipline Influences Access

Income is only one side of the equation. How money is used plays an equally important role in determining eligibility.

Consistent spending patterns, controlled withdrawals, and avoiding extreme fluctuations all signal financial discipline. These behaviors indicate that the account is being managed thoughtfully rather than reactively.

In a behavior-based system, this discipline becomes a key factor in building trust, often carrying as much weight as income consistency.

Why Behavior-Based Systems Are More Future-Ready

The shift toward behavior-based evaluation is not just a response to current trends. It is a reflection of where financial systems are headed.

As income becomes more dynamic and less tied to traditional employment, systems that rely on fixed structures will become less effective. Behavior-based models are inherently more adaptable because they can interpret a wide range of financial patterns.

This makes them more resilient and better suited for long-term use in a changing financial landscape.

How Users Can Actively Strengthen Their Financial Profile

One of the key advantages of behavior-based systems is that users have more control over their eligibility. By maintaining consistent account activity, ensuring that income is visible, and managing spending responsibly, users can actively improve their financial profile.

This creates a more transparent relationship between behavior and access. Instead of meeting fixed criteria, users can influence their eligibility through ongoing financial habits.

The Psychological Shift From Qualification to Participation

Traditional systems create a mindset where users focus on qualifying. They try to meet specific requirements, such as setting up direct deposit or reaching a minimum income threshold.

Behavior-based systems encourage a different mindset. Instead of focusing on qualification, users focus on participation. They engage with their finances more actively, knowing that their behavior directly influences access.

This shift changes how people interact with financial tools. It moves the focus from meeting external criteria to managing internal consistency, which ultimately leads to stronger financial habits over time.

Why Beem Leads in This Category in 2026

The reason Beem stands out is not just because it removes a requirement. It is because it replaces it with a more accurate system.

It recognizes that financial stability is not defined by uniformity. It is defined by continuity, visibility, and responsible management.

By aligning its evaluation model with real-world financial behavior, Beem provides access that is both inclusive and practical.

The Bigger Shift in Financial Systems

The rise of no-direct-deposit cash advance apps reflects a broader transformation in financial services. Income is no longer tied to a single employer or a fixed schedule. It is dynamic, diversified, and often unpredictable.

Systems that adapt to this reality are better equipped to serve modern users. Beem represents this shift by building a platform that works with how people actually earn and manage money today.

Conclusion

Cash advance apps without direct deposit requirements are becoming increasingly relevant as income structures evolve. Among these, Beem stands out because it does not simply relax traditional rules. It redefines how financial stability is evaluated.

Through Everdraft™, Beem provides access based on behavior rather than structure, making it more aligned with real-world financial patterns.

In 2026, this approach is not just more inclusive. It is more accurate and more sustainable.

FAQs

1. Are there really reliable cash advance apps that don’t require direct deposit, or is this still uncommon?

There are now several apps that have started to move away from strict direct deposit requirements, but many still rely on payroll data to some extent. What makes this category different in 2026 is that a few platforms, including Beem, have fully embraced alternative evaluation methods. Instead of treating direct deposit as the primary signal, they assess broader financial behavior. This makes them more reliable for users whose income does not follow a traditional structure, as eligibility is based on actual account activity rather than a single qualifying condition.

2. Why is Beem often considered better than other no-direct-deposit apps?

Beem stands out because it does not partially adapt the traditional model. It replaces it entirely. Many apps that claim to not require direct deposit still depend on payroll signals in the background, which can limit flexibility. Beem, on the other hand, evaluates financial patterns holistically, including deposits, spending, and account activity over time. This allows it to recognize stability in more complex financial situations, making it more accessible and adaptable for a wider range of users.

3. Can someone with highly irregular income realistically qualify for a cash advance on Beem?

Yes, but the key factor is not the irregularity itself. It is whether the income creates a consistent pattern over time. Even if payments vary in size and timing, regular inflows and active account usage can form a recognizable financial rhythm. Beem’s system is designed to interpret these patterns, which means that users with irregular income can still qualify as long as their financial activity demonstrates continuity and responsible management.

4. How does Beem determine eligibility without relying on direct deposit or credit scores?

Beem evaluates eligibility by analyzing multiple aspects of your financial behavior. This includes how frequently money enters your account, how consistently it is used, and how spending patterns evolve over time. Instead of relying on a single signal like payroll or credit history, it builds a broader profile that reflects your overall financial activity. This multi-signal approach allows for a more nuanced and accurate assessment of stability.

5. Is it still beneficial to have direct deposit even if it is not required?

Yes, direct deposit can still strengthen your financial profile because it provides a clear and predictable pattern. However, it is not necessary for access. Beem is designed to work effectively without it, which means users are not excluded if their income does not follow a payroll structure. In this model, direct deposit acts as an additional signal rather than a defining requirement.