Key Summary

You need to access $200. Someone’s sending it to you, or you’re withdrawing from your account. The question is: Do you want it as a gift card or should you hit the ATM for cash? Gift Card Withdrawals vs ATM Withdrawals.

Ten years ago, this wasn’t even a question. Money meant cash. Withdrawals meant ATMs. That was it. Now? You have options. And those options come with different costs, speeds, levels of flexibility, and use cases.

Let’s understand the real differences between gift card withdrawals and ATM withdrawals so you can make the smart choice for your situation.

What Each Type of Withdrawal Actually Means

Before we compare them, let’s make sure we’re talking about the same things.

Gift Card Withdrawals Explained

A gift card withdrawal means receiving money as store credit instead of physical cash. It’s digital or physical purchasing power tied to specific retailers.

You get a code emailed to you or a plastic card delivered. That code or card holds a value you can spend at Amazon, Walmart, Target, gas stations, restaurants, or wherever the card is designated.

ATM Withdrawals Explained

An ATM withdrawal is the traditional method. You have money in a bank account or on a prepaid card. You go to an ATM, insert your card, enter your PIN, and the machine dispenses physical cash.

That cash is in your hand. You can fold it, count it, and put it in your wallet. It’s a universally accepted currency you can spend anywhere.

The Fundamental Difference

Gift cards give you digital value for specific vendors. ATM withdrawals give you physical currency in a universal format. One restricts where you can spend. The other allows spending anywhere. Both convert stored value into usable form. They just do it differently.

Speed: Which Gets You Money Faster?

Let’s talk about how quickly you can actually use the money.

Gift Card Withdrawal Speed

Digital gift cards are instant. Someone sends you an Amazon gift card right now, and it’s in your email within 30 seconds. You can start shopping immediately.

Physical gift cards take 1-2 days to ship to you, but most gift card “withdrawals” are digital codes these days. Once you have the digital code, you can use it online immediately. For in-store use, it’s as fast as you can get to the store. No waiting. No processing. Just instant availability.

And there’s no line. No waiting behind three people at an ATM.

ATM Withdrawal Speed

An ATM withdrawal takes 2-3 minutes at the machine. Insert card, enter PIN, select amount, wait for cash to dispense, take cash and receipt.

But that doesn’t account for getting to the ATM. If there’s one across the street, great. If you need to drive 10 minutes, that’s travel time. If the ATM is busy, you’re waiting in line. If you need more cash than one withdrawal allows, you’re doing multiple transactions.

Once complete, you have immediate cash in hand. But the total time from “I need money” to “I have usable money” can range from 15 to 30 minutes, depending on location and circumstances.

Winner: Depends on Your Location

If you’re sitting at home and want to order something online, a digital gift card is faster. No travel required. You’re shopping for a minute.

If you’re already standing next to an ATM and need cash for something nearby, it’s faster. The speed advantage shifts based on context. Neither is universally faster.

Cost Comparison: The Fees Nobody Likes Talking About

This is where things get interesting.

Gift Card Fees (Usually None)

Most retail gift cards have zero fees. Someone sends you a $100 Walmart gift card, you get $100 worth of Walmart purchasing power. Full value. No deductions. There are no transaction charges. No convenience fees. No processing costs passed to you.

Some prepaid Visa or Mastercard gift cards have activation fees ($3-6), but standard retail gift cards from stores like Amazon, Target, Walmart, and gas stations – these are free.

ATM Withdrawal Fees (Often Significant)

ATM fees are where your money disappears. If you use your bank’s ATM, you might pay nothing. Many banks offer free withdrawals at their own machines.

But use an out-of-network ATM and watch what happens:

- Your bank charges you: $2-3 for using someone else’s ATM.

- The ATM operator charges you: a $2-4 surcharge.

- Total cost: $4-7 for a single withdrawal.

International ATMs are worse, often $5-10 in combined fees.

The Real Cost Over Time

Let’s do the math that most people don’t think about.

Say you withdraw $100 every week at an out-of-network ATM. That’s $6 in fees per withdrawal (average).

Weekly: $6 Monthly: $24 Yearly: $288.

You’re losing almost $300 per year just to access your own money.

If you received that same $100 as a gift card for stores you shop at anyway, your cost would be $0. Full value preserved.

When ATM Fees Are Worth It

Sometimes the fee is worth paying. If you need cash for a cash-only situation, you don’t have a choice. If you’re tipping a service provider, they need physical money. If you’re paying rent with a money order, you need cash to buy it.

Convenience has value, too. If driving to your bank’s free ATM takes 30 minutes, but there’s an out-of-network ATM 2 minutes away, the $4 fee might be worth your time.

But for routine spending at major retailers? The gift card’s zero-fee structure saves significant money.

Accessibility: Where and When You Can Use Each

Let’s talk about practical access to your money.

Gift Card Accessibility

Gift cards are limited to specific retailers or networks. An Amazon card only works on Amazon. A Shell gas card can only be used at Shell stations. A Walmart card only works at Walmart.

But within those limitations, accessibility is broad. Amazon has 300+ million products. Walmart sells groceries, clothing, household items, electronics, and pharmacy items. Gas cards work at thousands of locations nationwide.

Online gift cards work 24/7 from anywhere with an internet connection. In-store gift cards work during business hours. No geographic limitations for online shopping.

ATM Accessibility

ATMs require you to physically go somewhere. Your bank might have branches and ATMs nearby. Or they might not.

In urban areas, ATMs are everywhere. In rural areas, you might drive 15-20 minutes to find one. Some ATMs operate 24/7. Others have limited hours based on the location they’re in (grocery stores, gas stations).

Acceptance After Withdrawal

Here’s the critical difference:

Gift cards are valid only at their designated retailers. They fail for bills, rent, most services, and cash-only businesses.

Cash works everywhere. Every business. Every person. Every situation. Complete universal acceptance. This flexibility gap is massive. Cash provides options that gift cards simply cannot.

Bank Account Requirements

This matters more than most people realize.

What You Need for ATM Withdrawals

You need a bank account or a prepaid card that has ATM access. You need a valid ATM or debit card. You need to know your PIN. Your account must have sufficient funds. It must be in good standing (not frozen or closed).

If you don’t have a bank account, ATMs are completely inaccessible to you. You’re locked out of the entire ATM system.

What You Need for Gift Card Withdrawals

You need an email address or a phone number to receive digital gift cards. That’s it. No bank account required. No credit check. Usually, there is no identification. No minimum balance. No monthly fees.

This accessibility is huge for the 6 million American households without bank accounts.

Security Considerations

Both methods have security risks. Let’s be real about them.

ATM Cash Security Risks

Physical theft is the obvious one. Pickpockets, mugging, lost wallets. Once cash is stolen, it’s gone forever. No recovery. No insurance.

ATM skimming devices steal card information. Criminals install cameras to capture PINs. Shoulder surfing at ATMs is common in busy areas.

Carrying large amounts of cash is risky. $1,000 in your wallet is a target and a vulnerability.

Gift Card Security Risks

Digital codes can be hacked or phished if you’re not careful. Email accounts can be compromised. If someone gets your gift card code, they can use it.

Physical gift cards can be stolen and used like cash. Lost email access means lost codes unless you backed them up elsewhere.

There’s no FDIC insurance on gift cards. If something goes wrong, recovery is difficult and often impossible.

However, some gift cards can be replaced if you have the receipt and original purchase information. That’s better than cash.

Which Is Safer?

Small amounts of cash ($20-50) are relatively safe to carry. Large amounts of cash are very risky. Digital gift cards are safe if you manage them properly (screenshot codes, back them up, and use secure email). Both require careful management. Neither is perfectly secure. Therefore, the smartest approach is diversification. Don’t keep all your money in one form.

Making the Choice: Gift Card or ATM?

Here’s your decision guide:

Choose Gift Cards When:

- Shopping at major retailers (Walmart, Target, Amazon)

- Buying gas at specific chains you use regularly.

- You want to avoid ATM fees.

- Shopping online from home.

- Using a budgeting system with category spending limits.

- You don’t have a bank account.

- You know exactly where you’ll be spending the money.

Choose ATM Cash When:

- Paying bills that require money orders.

- Need cash for small businesses.

- Tipping service providers (hairdressers, servers, delivery drivers).

- Buying from individuals (garage sales, private transactions).

- You need maximum flexibility and aren’t sure where you’ll spend.

- Cash-only situations (some restaurants, markets, services).

- Paying rent to landlords who want cash or money orders.

The Hybrid Approach That Actually Works

Smart people don’t pick just one method forever. They use both strategically.

Use gift cards for predictable retail spending. Groceries, gas, household items, known expenses. Capture full value with zero fees. Keep some ATM cash for flexibility. Have $50-100 available for situations requiring cash.

Minimize ATM fees by withdrawing larger amounts less frequently. One $200 withdrawal monthly instead of four $50 withdrawals saves $12-24 in fees. Let gift cards handle routine purchases. Reserve cash for situations that require it.

This hybrid approach maximizes value while maintaining flexibility.

Also Read: How Secure Are Gift Card Withdrawals?

Platform Flexibility Matters

Here’s where modern money transfer gets smart.

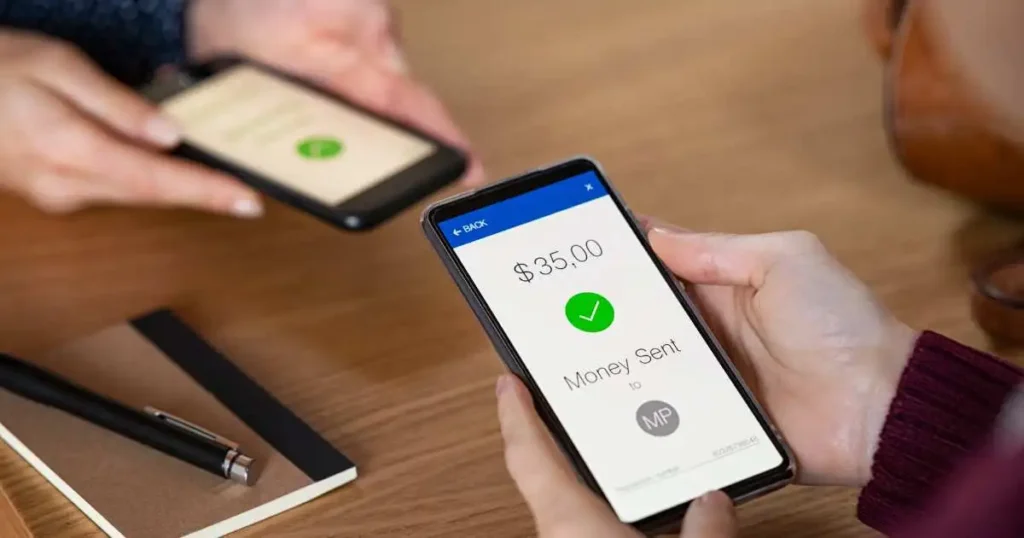

When someone sends you money through Beem, you get to choose your withdrawal method. Gift cards to popular retailers, or cash to your debit card or bank account. The sender isn’t deciding for you. You assess your immediate needs and choose the format that best suits you.

Need groceries this week? Choose a Walmart gift card and keep the full value with zero fees.

Need to pay rent? Choose cash withdrawal to your bank account.

Not sure what you’ll need? Choose cash for maximum flexibility.

Different needs at different times call for different formats. This month, you need cash for bills. Next month, you’re doing a big grocery shop, and gift cards make more sense. The following month, things are uncertain, and cash feels safer.

Flexibility prevents wrong choices. You’re not locked into one format that might not solve your actual problem.

The Honest Limitations of Each

Let’s not pretend either method is perfect.

What ATM Withdrawals Cannot Do?

- They can’t eliminate fees at out-of-network ATMs. Those fees are real, and they add up.

- They can’t be used safely for large amounts. Carrying $2,000 in cash is dangerous.

- They can’t be recovered if lost or stolen. Cash is gone forever.

- They can’t work without a bank account. No account means no ATM access.

- They can’t avoid the need to physically go somewhere to get the money.

What Gift Card Withdrawals Cannot Do?

- They can’t pay rent or most bills directly. Landlords and utility companies don’t accept gift cards.

- They can’t work at cash-only businesses. If a place only takes cash, your gift card is worthless.

- They can’t be used for tipping. Service workers need physical money.

- They can’t provide universal flexibility. You’re restricted to specific retailers.

- They can’t be saved in traditional bank accounts that earn interest.

Accepting the Trade-Offs

No perfect solution exists for all situations. Each tool serves a specific purpose. Smart money management means understanding these limitations and making informed choices accordingly. You’re not trying to find one universal answer. You’re trying to match the right tool to each specific job. Sometimes that’s gift cards. Sometimes that’s ATM cash. Often it’s a combination of both.

Also Read: What are the Different Ways to Send Money in the US?

The Bottom Line

Gift cards and ATM withdrawals aren’t competing options; one isn’t always better. They’re different tools for different jobs. Gift cards win on cost, speed for online shopping, and accessibility. ATM cash wins on flexibility, bills and services, and universal acceptance. Neither method is superior in all situations – the winner changes based on what you’re actually using the money for.

The smartest money management approach uses both strategically: gift cards for predictable retail spending at major chains where you preserve full value with zero fees, and ATM cash for everything else, including bills, services, cash-only businesses, and situations requiring maximum flexibility.

Platforms that offer a choice between gift cards and cash withdrawals (like Beem) make sending money just as seamless as spending it. Whether you’re transferring funds to someone instantly or choosing how to receive them, Beem helps ensure the process stays quick, flexible, and suited to real-life needs. Need groceries at Walmart? Gift card saves fees. Need to pay rent? Only cash works. Choose wisely, choose strategically, and don’t be afraid to use both when the situation calls for it.

FAQs About Gift Card Withdrawals vs ATM Withdrawals

Are gift cards better than ATM withdrawals?

Neither is universally better – it depends on your specific need. Gift cards are better for shopping at major retailers because they have zero fees and preserve full value. ATM cash is better for paying bills, tipping, cash-only situations, and anything requiring maximum flexibility. For someone who does weekly grocery shopping at Walmart, a gift card saves $200-300 in ATM fees each year.

How much do ATM withdrawals actually cost compared to gift cards?

Out-of-network ATM withdrawals typically cost $4-7 per transaction ($2-3 from your bank plus $2-4 ATM surcharge). If you withdraw $100 per week at out-of-network ATMs, you’ll pay about $288 in fees annually. Gift cards for the same retailers typically have $0 fees, giving you full face value.

Can you get cash from a gift card like you can from an ATM?

No, with rare exceptions. Standard retail gift cards (Amazon, Walmart, Target) cannot be used to withdraw cash at ATMs. Only prepaid Visa or Mastercard cards that specifically state “ATM access” allow cash withdrawals, and these charge $2-3 per withdrawal plus ATM operator fees.

Which is faster: a gift card or an ATM withdrawal?

Digital gift cards are instant (30 seconds to email, immediate use online), while ATM withdrawals take 2-3 minutes at the machine plus travel time to reach the ATM. However, “faster” depends on your situation.

Do you need a bank account to withdraw gift card funds?

No, you don’t need a bank account to receive or use gift cards. You only need an email address or phone number for digital gift cards. This makes gift cards accessible to the 6 million American households without bank accounts.